All Newsletters

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

eServe Newsletter January 2012

eServe wishes you...

A happy & prosperous New Year!

Will the life insurer honour the claim in the event of your death?

Published: Wednesday, Jan 11, 2012 | By Vishal Shah | Agency: DNA

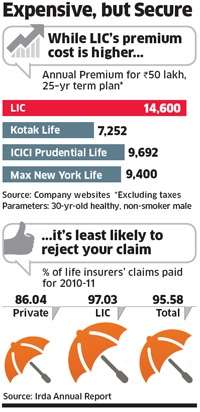

There is a tendency among people to opt for a life insurer which charges lesser premium. However, besides the premium, the two other important things one should consider before choosing an insurer are the probability of getting the claim settled in the event of the death and the time taken to settle the claim.

Nobody will like to be in a situation where one has paid the premium diligently for 20 years and after his death, the claim is disapproved for any reason. One will also not like to be in a situation where his family gets the insurance proceeds after six months or say even after one year of the death. Hence, it is necessary to do an analysis of claims settled by insurance companies.

Claim settlement analysis

The accompanying tables (I & II) lists the best-five and the bottom-five life insurance companies in terms of claim rejection for the year 2010-11. The best companies have the least claim rejection ratio whereas bottom five companies have the highest claim rejection ratio. The list is broken down into how old these rejected policies were when the death occurred. Older the policies less should be the chance of rejection.

LIC is the best among the entire lot of insurance companies with only 1% of the claims getting rejected. ICICI Prudential and Kotak Life are among the private insurance companies making it to the best five listing.

Aegon Religare tops the list of bottom five companies with 45 out of every 100 claims rejected during the period under review. Shriram Life, Future Generali Life, IDBI Federal and DLF Pramerica are other insurance companies which have claim rejection ratio of greater than 20%.

If we notice the age of the policies for which claims are rejected, most of them are less than two years old. In the case of Aegon Religare, all the claims rejected are for policies less than two years old.

The relevance of two years is insurance company cannot reject claims for such policies on the basis that the policy was taken based on misrepresented facts, unless the insurance company shows that such misrepresentation was material and fraudulently made and the policyholder knew that he was misrepresenting a material fact.

Thus, generally unless proved otherwise by the insurer, claim pertaining to policies more than two years old should get settled. However, it does not mean that any claims made within first two years should be rejected. Such claims can go for additional scrutiny, but should get settled if found in order.

Thus it becomes interesting to know the companies which have rejected most numbers of claims for policies greater than two years.

For example, SBI Life has rejected 17 out of every 100 claims made. About 42% of such rejected claims are for policies in force for more than two years. There has to be very compelling reasons to reject such claims and it shall be interesting to know the reasons.

It shall also be interesting to know how many of the claims made within first two years of the policy are settled. Unfortunately, the insurance companies are not mandated to provide such details.

Another way to look at the claim rejection ratio is to check whether such high rejection ratios are a one-time event or a regular feature. Looking at the claim rejection ratio for all life insurance companies for the last two years, one can notice that there has not been substantial difference in the two years. Many companies have rejected more claims in 2010-11 as compared to in 2009-10.

Claim turnaround time

Let us define claim turnaround time as the number of days taken to settle claim once all the documents are submitted to the insurance company. Usually, once all the documents are submitted, the insurance company should be quick in settling the claim either ways.But if you think so, wish you good luck.

There are insurance companies where more than 50% of the claims submitted are outstanding for more than three months. Sahara has the worst turnaround time followed by Future Generali Life and Shriram Life.

Conclusion

LIC stands out with the lowest claim rejection ratio and also a decent turnaround time. In the private sector, Kotak Life and ICICI Prudential have low claim rejection ratios. Kotak Life is better than ICICI Prudential in rejecting claims for policies in force for more than two years, whereas ICICI Prudential scores over Kotak Life in claim turnaround time.

Companies such as Aegon Religare and Star Union Daichi have started operations in last 2-4 years and we need to give them more time so that more sensible analysis can be carried out on their claim settlement details.

Thus, the cheapest plan available may not be the best one to opt for. One has to also look at the companys claim settlement ratio as well as claim turnaround time before zeroing in on the insurer.

The writer is a chartered accountant.

LIC lays claim to no.1 spot in settlements

Published: Dec 30, 2011 | Agency: Economic Times

Ahead of the rest Staterun insurer settled 97% of all claims,

private cos for behind

Life Insurance Corporation remained well ahead of private rivals in living up to the purpose of insurance by settling 97.03% of claims in 2010-11, helping the state-run giant retain its market dominance even a decade after its monopoly ended.

Settlement of claims at LIC rose from 96.54% in 2009-10, the Insurance Regulatory and Development Authority said in its annual report. For the private sector, where the premia on policies are lower than for LIC, the claims-to-settlement ratio was 86.04%, up from 84.87% in 2009-10.

Higher the ratio of settlement to claims, the more customer-friendly a company is. The regulator does not provide statistics for individual private firms.

"Insurers should take all steps to ensure the incidence of claim repudiation is reduced to the barest minimum," the regulator said in its annual report. "For this to happen, they should adopt measures to explain to the parties upfront the exact coverage and exclusions."

LIC, which controls nearly three-fourths of the market, scored on another front: its repudiation of claims declined to just 1% in FY11, from 1.21% a year earlier. The remaining claims are under dispute. For private life insurers, repudiation rose to 8.90% of claims from 7.61% in FY10.

Settlement of claims is the key factor that decides customer satisfaction and a company's profitability. While genuine claims are usually settled by both private insurers and LIC, private players see more disputes. Stricter due diligence means more fake claims are detected at private companies, while LIC is relatively lax in rejecting fake claims, reducing its profitability.

"Insurance is not what you sell, but deliver," said AK Dasgupta, MD, LIC. "People trust LIC because of our strong claims settlement record. They know we have the ability because of our balance sheet and intention. People need insurance for two reasons - uncertainty and good return."

In 2010-11, life insurance companies settled 8.13 lakh claims on individual policies, with a total payout of Rs 7,595 crore. As many as 17,350 claims amounting to 336 crore were repudiated.

New Stock Market Report Triggers Panic

This morning has been unusually busy... for TV anchors.

There's a new report out which predicts that the BSE Sensex could hit 11,000.

And TV anchors are doing their best to whip up panic based on it.

Just ignore all this 'noise'...

Stock markets rise, and fall. This is a given.

But what matters to you is where stock markets are in say 3 years or 10 years for that matter.

And when it comes to that, things could not look better.

Why?

Well the present stock market crisis has thrown up exciting money making opportunities, and in particular these select Blue Chip stocks that are available for dirt cheap.

- SIP Is the Best Product for this scenario.

- A Financial Consultant is the Right Person to ask for A Right Advise.

- Asset Allocation will play a vital role.

- Last But Not The least -People who time the market will Loose the Most.

- People should Invest by way of Sip.He will be the Wise Investor.

As per the Reserve Bank Of India (RBI), the banks have nearly Rs 900,000 crores tied up in risky sectors that include these sectors. The sectors have seen their earnings come under pressure due to higher costs of input as well as increasing interest rates. As a result, risk associated with the loans to the companies in these sectors has been increasing. The risk is evident in the fact that the bad loans of the Indian banks have gone up nearly 33% in the quarter ended September 2011.

More and more banks are increasing their provisioning as well as reporting higher NPAs (non performing assets) in recent times. As per RBI, the total loan portfolio of the banks is heavily inclined towards the risky sectors. Nearly one fifth of the total loan portfolio of banks consists of loans to risky sectors.

It is not that all the risky assets would end up becoming nonperforming assets (NPAs). But these loans have increased the riskiness of Indian banks, particularly the public sector banks. The increased risk would call for increase in capital for these banks. This in turn would mean the government would have to provide for the additional capital requirements in its budget which would further worsen India's burgeoning fiscal deficit. This would deepen the existing negative sentiment in the country.

To add to this, the banks themselves would prefer to become stricter when it comes to scrutinizing and granting new loans. This in turn would further worsen the country's economic situation as more and more sectors which rely on credit to fuel expansion plans would see funds drying up. This would further worsen the slowdown that has already gripped out economy.